The seeds of Britain’s biggest welfare overhaul in a generation were planted in Glasgow's east end. The epiphany that then-Conservative leader Iain Duncan Smith had during a gloomy 2002 visit to the sprawling, post-war Easterhouse estate—an area plagued by poor infrastructure and a pervasive sense of despair—sparked a chain reaction to "make work pay."

Today, that vision has evolved into Universal Credit, a massive system supporting over eight million people. However, as the rollout finally approaches the finish line—nine years late and vastly over budget—the program is wrestling with a completely new set of crises.

The demographics of unemployment have shifted dramatically. The Centre for Social Justice (CSJ) reports a 46% surge in unemployed graduates claiming benefits since 2019, totaling 700,000 individuals. Furthermore, mental and behavioral issues now account for nearly half of all incapacity claims, double the rate seen during Duncan Smith's initial Easterhouse tour.

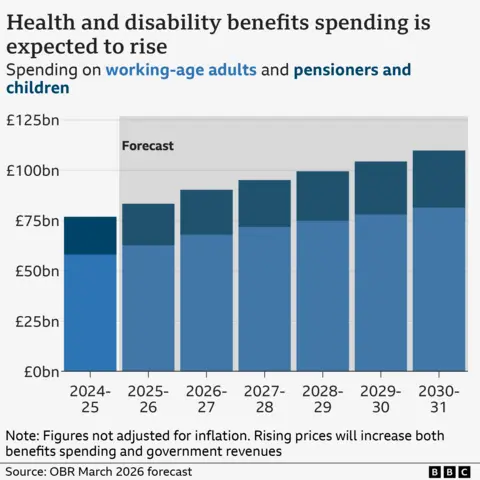

These shifting dynamics are driving costs skyward. By 2029, annual spending on health and disability benefits is projected to rocket from £65 billion to £100 billion. The government now admits the current setup inadvertently rewards sickness, prompting another wave of reforms. But can a system originally designed simply to incentivize employment adapt to this complex reality?

The Struggle to Make Work Pay

When Duncan Smith conceived the system, the goal was simple: eradicate the "destination" mindset of welfare and turn it into a stepping stone.

The strategy involved combining six working-age benefits into a single monthly payout, stripping away the complex math that previously discouraged claimants from taking jobs. Joe Shalam, a former Department for Work and Pensions (DWP) adviser, notes that Universal Credit was globally recognized as a massive upgrade that restored employment incentives. By 2019, officials claimed these reforms had reduced workless households by a million over nine years.

Debt Traps and the Five-Week Wait

However, the modern realities of Universal Credit have been heavily criticized. Following a four-year freeze on working-age benefits starting in 2015, the actual purchasing power of the payments plummeted. Anti-poverty advocates argue this erosion—coupled with the system's fundamental design flaws—has fueled a historic reliance on food banks.

A major friction point is the mandatory five-week wait for an initial payment, designed to mimic a monthly paycheck. Since many vulnerable households lack savings, they are forced to take interest-free DWP advances. These loans are automatically deducted from future payouts for up to two years, creating an immediate cycle of debt.

Citizens Advice warns that the policy requires urgent reform. Policy manager David Mendes da Costa points out that a safety net should not trap claimants in debt from day one, yet that is exactly what welfare advisers witness daily. For example, young adults under 25 receive a meager £317 monthly standard allowance. Claimants argue that this sum forces reliance on parents and fails to provide a viable path to financial independence as an adult.

A Perverse Incentive

There is a growing consensus among welfare experts that the standard Universal Credit rate is simply insufficient to survive on. This financial desperation may be pushing more claimants to seek the system's health-related supplements. A recent government paper acknowledged that the low baseline creates a "perverse incentive" to apply for the health element, which pays an additional £423 a month to those over 25 on top of their standard £400 base allowance.

Tragically, those who secure the health top-up often lose out on vital employment support, inadvertently sidelining people who might otherwise want to work.

To combat this imbalance, ministers are planning a major adjustment. Starting in April, the basic allowance will jump by a robust 6.2%—surpassing inflation—with sustained increases planned through the end of the decade. Simultaneously, the government intends to slash the health top-up by half for most new applicants. By the close of this Parliament, analysts at the Institute for Fiscal Studies project these adjustments will fundamentally alter the financial calculus for millions navigating the UK's welfare safety net.